Charging infrastructure gets a foothold in the country

EV adoption in India is caught in a chicken-and-egg warp, leaving it to the government to take the lead and promote an EV ecosystem. And hence, Energy Efficiency Services Ltd (EESL) launched the national e-mobility program in 2018 to provide impetus to Indian manufacturers in the e-mobility space by gaining efficiencies of scale, creating local manufacturing facilities, and growing technical competencies for the long-term growth of the EV industry in India. This has been achieved by aggregating demand for EVs and charging infrastructure from various government departments for which 200+ Public EV Charging Stations (PCS) have already been installed around 1514 EVs, and 463 captive chargers deployed across the country.

EESL is a joint venture of four public sector undertakings, NTPC Ltd, POWERGRID, Power Finance Corporation and REC Ltd. Convergence Energy Services Ltd (CESL) is a hundred percent owned subsidiary of EESL, created primarily to focus on EVs, charging infra, and decentralized solar power projects.

Decarbonization, decentralization, digitalization

A glance at the conventional energy market, relative to the transforming future market, shows centralized power generation facilities veering to demand-side power transactions. Future energy transactions are conducted from the position of a strengthened democracy with greater public participation and local energy ownerships. The distribution utility would now act more as an operator due to multiple decentralized generation facilities, which could independently service multiple sectors - such as the business, the industrial, or the household sector.

The case for RE is compelling with the lowest bid received for solar to date at ₹2 per kWh and even lower bids being possible. This is particularly relevant as TERI predicts the cheapest variant of coal shortly to be in the range of ₹6.98 per kWh. India shows a commendable record of shifting to green energy with about 50 percent of power capacity addition in India since 2015 being renewable. This places the country in a favorable position to link RE with EV charging infrastructure (EVCI). Both State and Central governments encourage the integration of renewables with EVCI in their EOIs and subsidy schemes.

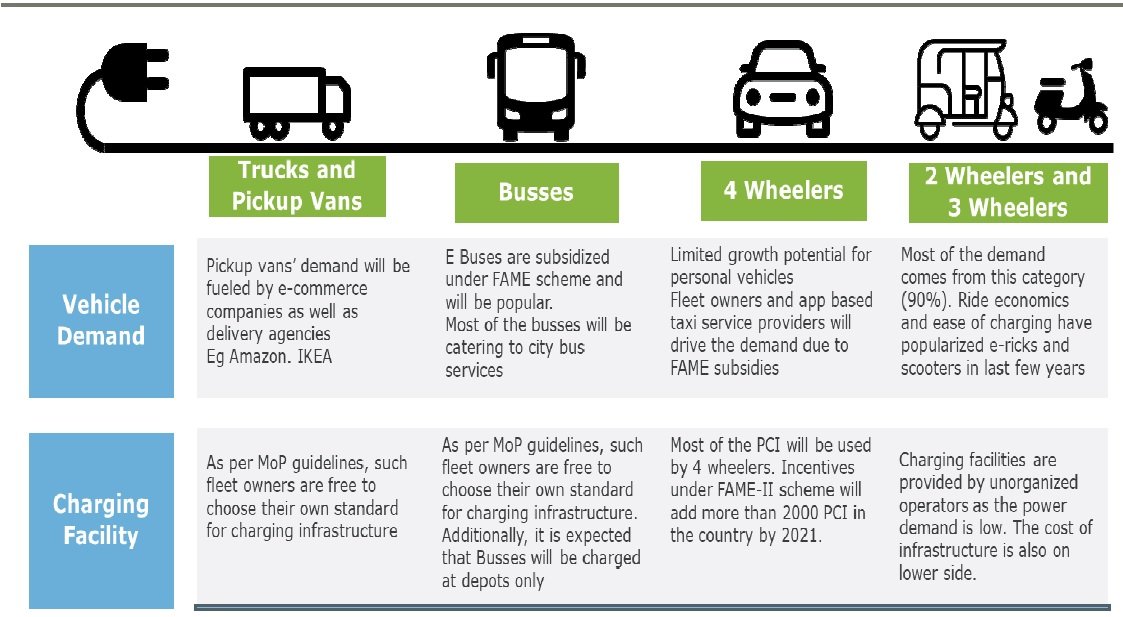

Zero tailpipe emissions from EV transport can significantly reduce carbon emissions on a country-wide scale. The high savings compared to ICE vehicles will drive a clear demand from e-commerce companies and logistic applications for e-mobility. Electric buses being more subsidy-driven will be popular as city bus services to an extent. In the car segment, the initial demand will be driven by commercial fleet operators and app-based taxi services, incentivized by State and Central subsidies. In the 2W and 3W segments, ride economics will pull off around 80 percent conversion. The e-3W electric rickshaw category is a success story in India even without a subsidy in place.

In a study done by researchers based at Cambridge University, it was ascertained that EVs have lower lifecycle emissions compared to ICE vehicles. Besides, if the source of electricity generation is renewable, there is a significant opportunity to further lower emissions.

Lifecycle emissions (global average of 59 countries)

Petrol car: Average 305 gCO2eq/vehicle KM

Electric car: Average 213 gCO2eq/vehicle KM

Electric car: 75 gCO2eq/vehicle KM (largely renewable- and nuclear-powered, Switzerland)

Charging infrastructure will evolve as per each EV segment: the pickup van and delivery segment will rely largely on their own charging facilities known as the captive charging variety. The FAME II subsidized e-buses with a pre-fixed route will also utilize captive charging at depots and the destination locations. It is the personal vehicle segment that will drive the demand for public charging stations. The incentives fall under the FAME II scheme, and around 2000 public charging infrastructure stations (PCI) will be set up under subsidy by 2021. The highest segment of EVs - the 2W and 3W - are serviced by the non-formal sector and home charging.

Demand projections for EV charging stations

If one were to estimate a volume close to at least 100 million EV sales, and factor in just the 4W segment, it would translate to 10 million EV sales by 2030. So even considering the absurd assumption of 10 vehicles to one charging station, we would be looking at one million charging points by 2030. These would require a combination of both AC and DC charging ports. Initially, at least 30 percent will be DC fast-charging stations and the balance 70 percent will be slow charging points.

To promote the early adoption of EVCI, user profiles that rely on different technologies to serve an individual segment's needs should be identified

India is majorly promoting e-mobility, and as with all nascent industries, it faces some inherent challenges for the development of an EV ecosystem. Listed broadly, one for sure is the high upfront cost of EVs; the second is the shortage of EV model types and the third is the lack of charging infrastructure.

Compared with the ICE vehicle, the e-car presently sells at a premium. Thus, FAME II enables financial incentives to OEMs to help reduce the cost of EVs. The subsidy is based on the battery capacity of the EVs. So, for e-2W, -3Ws, and -4Ws, ₹10,000 per kWh is the extent of subsidy.

The second major obstacle that limits the purchase of EVs is the paucity of options in EV models. ICE vehicle companies are offering top choices with a range of vehicles based on budget. Limited EV model options have OEMs launching newer vehicles in the market.

The foremost point remains the lack of charging infra, presently caught in a chicken and egg kind of scenario. Added to that is the high initial investment involved in setting up public charging stations; high land cost is also a major concern. These are some of the three broad eco-system challenges which need to be addressed if e-mobility has to expand its footprint in the country.

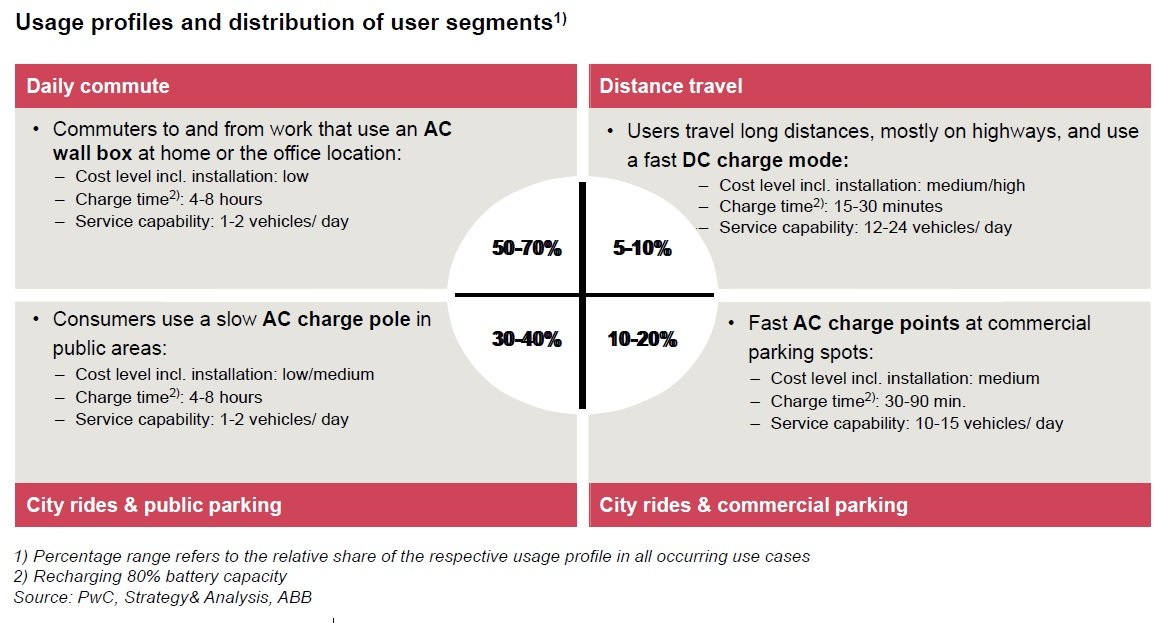

An interesting user profile study of charging patterns was done by consultants. In a daily pattern of users, one sees that close to 70 percent of daily commuters charge at home or their office locations. Close to 10 percent are distance travel usage profiles that require DC fast charging for a quick tank-up. Around 30 to 40 percent of consumers, who rely on slow or AC charge zones, especially in a public car park, are typically ones who do city rides.

So, from the user profile, it is very clear that almost 70 percent still rely on home charging or workplace charging facilities. The balance 30 percent would have access to a mix of AC slow charging and AC fast charging and DC fast charging modes. The DC fast charging mode would have about 10 percent demand.

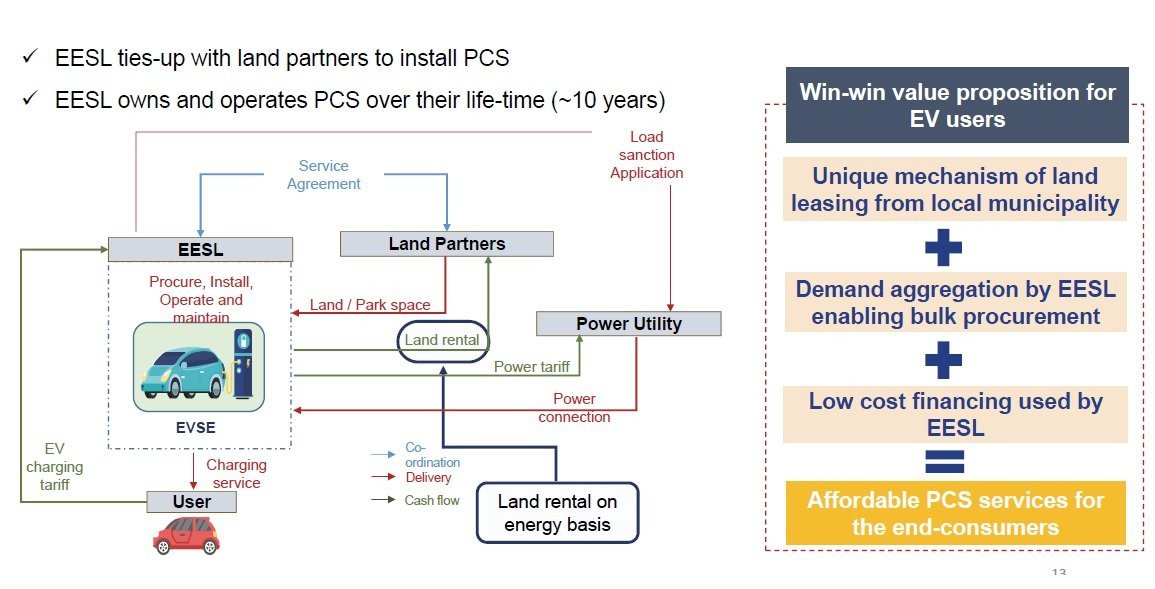

As per the business model of EESL for building EV charging stations, the company enters into a service agreement with the land partner. EESL and CESL build the stations with the complete investment whereby the land leasing, installation, operation, and maintenance are done by the company. Revenues are realized over a period The Usage Profile in Figure 2 helps analyze the type of infrastructure needed for EVs and the most profitable locations one could look at for setting up public charging infrastructure (PCI).

In addition to the usage profile study, EESL follows a scientific approach before setting up charging stations: a city is demarcated into a grid of 3x3 km as per Ministry of Transport guidelines. A secondary assessment brings up the city layout and points of public interest like bus depots, metro locations, worship places, the commercial establishments. This clarity obtained from the second assessment leads to a physical survey at the ground level, which constitutes a primary study of the individual sites. Now, the joint survey team is also involved, necessitating a different set of parameters like footfall, the density of the locations, load availability, visibility, and proximity to points of public interest.

These parameters are captured in the location assessment study. The feasible locations are demarcated into Priority 1, 2, and 3; priority 1 locations requiring minimum cost due to minimum intervention and so on. EESL then takes up the execution and operation and simultaneously evaluates the sustainability of the business. A close connection is maintained with OEMs and fleet operators so that they can use this public infrastructure to help monetize the charging asset quickly.

The need now arises for a study of the locations. If one looks at the usage concerning utilization time, one can assume around a 10 percent utilization factor in public charging stations of lower capacity chargers. For higher capacity, the utilization is around 5–7 percent. The point to note here is that even at 10 percent utilization there is no benefit to pass on in the service fee to EV users. Only at around 40 percent utilization is there scope for reduction in service fee by 44 percent. So, it becomes an important factor to assess locations to ensure high utilization of the PCS and viability in the business model.

Apart from the utilization, the study also helps in ascertaining the costs involved in building these stations. On completing an assessment, one can calculate the cost for construction as well as for the power connection.

of time through charging services. Typically, EESL shares a percentage of revenue from the charging station with the land partners. The responsibility of procuring the connection from the utility, building the infrastructure is done by the company. The agreement is signed for 10 years, giving the land partner a better and viable proposition to operate the public EV charging station.

An inherent benefit of the EESL business model is that requirements across States are aggregated to come up with a single procurement, enabling the benefit of economies of scale. The company also works closely with the private land partners, as well as with some of the multilateral funding partners allowing better access to cross financing. These are some of the parameters which help in building the infrastructure more efficiently and consequently provide an affordable tariff for the end customer. So far, EESL has built close to 200 plus public EV charging stations that comprise 375 charging points and around 1226 leased capital charging station points for leased EVs.

If you look at consumption numbers till November 2020, EESL has been responsible for more than 2,66,000 units of electricity being consumed, with the number having reached close to 330,000 units currently. So, basically, the company has supported close to 1.5 million km of clean travel. The utilization graph below indicates how replacement has improved over time. When EESL commenced operations in May 2019, the utilization was less than 5 percent, increasing gradually to 10-15 and then to 20 percent month on month.

The real-time impact of the lockdown in April and May of 2020 brought utilization down to under 1 percent when the entire e-mobility fleet operators had halted operations. What is the reason for utilization to have picked up so dramatically over such a short time? This can be ascribed to the study of the most lucrative locations for building EV charging stations. The company has also realized that adhering to a partnership model is a vital element to help improve our utilization, so we consult with OEM partners, EV fleet operators, and startup companies to understand their charging needs. EESL then tries to build the PCIs as per the demand locations ensuring an increase in the utilization of the charging stations.

With its charging stations built up across India, EESL offers a corporate plan for fleet operators giving them access to the country-wide network of charging stations through a mobile app. This also provides feedback on the EV user's requirements concerning charging and subscription and concerning car requirements and accessibility. In trying to address these concerns, the company gradually realized that once it aligns interests with user requirements, it was able to increase utilization of its charging infrastructure month on month.

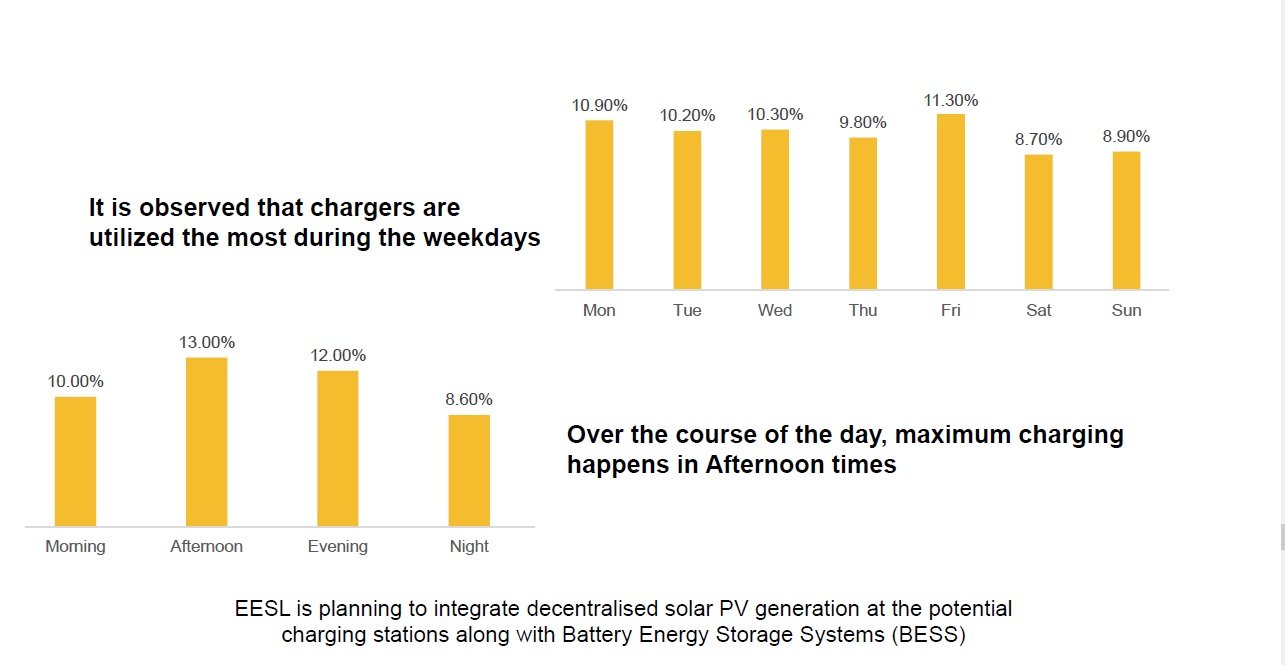

Weekly versus daily charging trends

Studying the utilization trend for a week shown in Figure 4 indicates a linear utilization close to around 8.5 to 10 percent, both on weekdays and weekends. Interestingly, however, the utilization trend in a 24-hour timeline indicates the bulk of utilization occurring in the afternoon and the evenings, and on a good note, also in the night time. On conducting a study with regular users such as commercial fleet operators, they said the reason for night-time utilization was due to easy accessibility of stations, primarily due to less traffic and more parking spaces.

The high or maximum charging in the afternoon indicates a great potential case for an aggregating solar generation along with a battery storage system. So, EESL is planning pilot projects on certain sites to capture solar generation with battery storage, without any incremental cost to EV customers.

Battery storage for RE

A typical schematic of an energy storage system: once we have multiple sources of generation at the public EV charging stations, then integrating the battery would be much easier. Here, the battery would help at least with storing the RE during the generation time and charging EVs as per demand. This prioritizes the usage of batteries for the storage of REpower. The excess power required for charging EVs would be supplied by the grid. Such prioritization will happen at select EV charging stations.

An interesting consumer study done by Deloitte focuses on the difference in consumer preferences concerning purchasing the next vehicle. Up to 50 or 51 percent of respondents have indicated clearly that they would like to go with diesel. When asked the reason behind this preference for an ICE vehicle, the response was due to the price factor. On questioning the consumer regarding willingness to pay extra for an EV, close to 53 percent said, if the price of the EV was less by ₹1 lakh compared to or close to an ICE vehicle, then 53 percent of consumers were willing to opt for e-mobility. So data indicates that price sensitivity is one factor, which will determine if a customer opts for an EV. Once the industry achieves a price matching that of ICE vehicles that would be the touchpoint from where EVs will take off.

On analyzing consumer willingness to spend time at EV charging stations, 35 to 50 percent said if the charging time is less than an hour, they were alright to recharge at the charging facility. EESL experience shows that public charging stations are AC fast-charging stations, where the consumers normally come for quick recharging. Typically, at these stations, the recharging time will be less than 30 minutes. Considering this, customers should find it convenient to utilize public charging stations, assisting in making EV a preferred choice as their next vehicle.

The blueprint that is revealing itself to establish charging infrastructure stations in the country, will build confidence in the industry to participate in a huge business opportunity. As it breaks the chicken and egg conundrum, EV adoption in India will take to the highways.

Spotlight